7 Reasons Why Goal Setting is the Foundation of Successful Financial Planning

Goal setting is the foundation of successful financial planning. Learn why clear, SMART financial goals drive wealth building, budgeting, investing & long-term success.

Financial planning without clearly defined goals resembles embarking on a cross-country journey with no destination. The process may initially seem enjoyable, but it ultimately leads to wasted resources, missteps, or stagnation. This happens because there is no direction.

The Three Layers of Financial Goals

The Three Layers of Financial Goals can be thought of as terraces, each one representing a different time horizon.Each layer builds on the previous one. A strong foundation in the early stages supports success in future financial goals.

- The short-term layer (0–3 years) includes building an emergency fund in a savings account, paying off credit card debt, and saving for a down payment in a high-yield account.

- The intermediate layer (3–10 years) covers goals such as setting up a college fund, saving for a future home, or putting aside money for a sabbatical or a second home.

- The long-term layer (10+ years) involves planning for retirement, creating a legacy fund, and contributing to philanthropic efforts.

Why Goal Setting is the Foundation of Successful Financial Planning

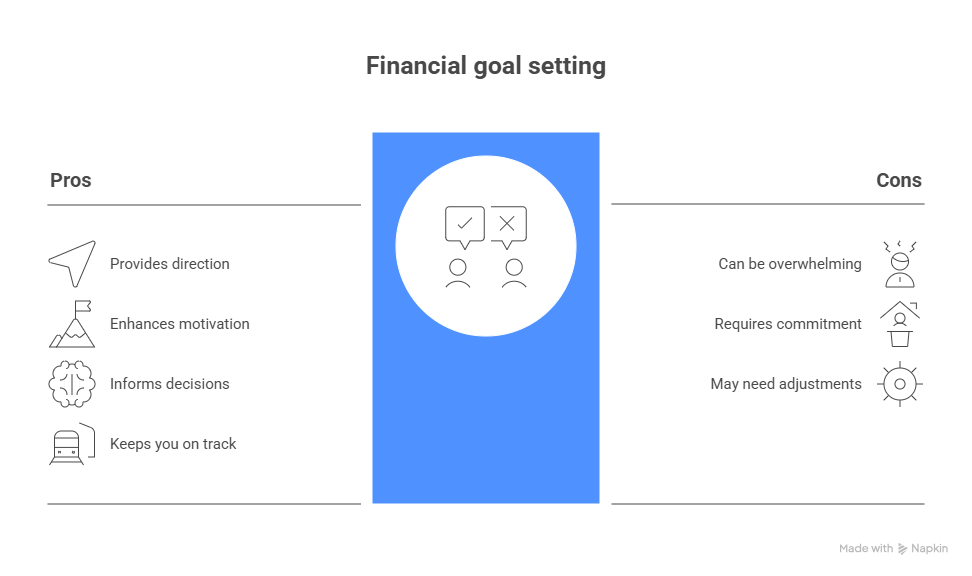

Goal setting is the most critical step in the financial planning process for the following reasons:

1. Goals provide direction and purpose for financial resources

Money is a tool, not an end in itself. Without goals, savings and investments lack purpose and coherence. Defining specific objectives—such as purchasing a home within five years, retiring at age 60 with $2 million, funding children’s education, or establishing a charitable foundation—turns unstructured saving into purposeful accumulation.

How goals provide direction and purpose for financial resources

- Goals act as a roadmap for money, telling you where to allocate resources instead of spending randomly.

- They prioritize spending and saving (e.g., emergency fund first, then vacation, then luxury purchases).

- Clear goals prevent lifestyle inflation and impulse buying by giving every dollar a “job.”

- Goals align financial decisions with life values (freedom, security, family, experiences, legacy).

- They motivate disciplined behavior like regular investing, cutting unnecessary expenses, and increasing income.

- Without goals, money lacks purpose → leads to aimless accumulation or wasteful spending.

- Regularly reviewing and updating goals keeps financial plans relevant as life changes.

2. Goals establish measurable milestones

These milestones allow individuals to track their progress and make necessary adjustments along the way. Each milestone serves as a checkpoint, providing motivation and clarity on how far one has come and what still needs to be accomplished. By breaking down larger goals into smaller, achievable targets, the financial planning journey becomes less daunting and more manageable. This approach not only fosters discipline but also encourages consistent saving and investment habits that align with overall objectives.

Goals establish measurable milestones. Vague aspirations, like wanting wealth, are not actionable. Specific and measurable goals—for example, accumulating $1.5 million by age 55—enable the development of detailed financial plans. An individual with this objective can calculate the required monthly savings. They can factor in current assets, expected returns, inflation, and choose strategies aligned with their timeline and risk. This turns abstract ambitions into actionable financial roadmaps.

3. Goals Turn Abstract Advice into Concrete Action

Your willingness to take risks should never be based solely on personality quizzes. It must be anchored to your goals and time horizon. A 30-year-old saving for retirement in 35 years can afford significant equity exposure. The same person saving for a house down payment in three years cannot. Clear goals foster an honest conversation about risk rather than emotional reactions to market swings.

4. Goals help prioritize competing financial demands.

Individuals often juggle simultaneous financial desires. These could include buying a new car, taking a vacation, upgrading a home, pursuing early retirement, or paying for private education. Goal setting requires ranking these objectives by importance and timeline. For example, someone may need to choose between allocating extra income to a family vacation or boosting retirement contributions. Establishing clear goals enables smart decisions about which objectives matter most. This prevents underfunding high-priority goals in favor of less important ones.

5. Goals provide motivation and discipline

Behavioral finance can be analyzed from a variety of perspectives. Stock market returns are one area of finance where psychological behaviors are often assumed to influence market outcomes and returns but there are also many different angles for observation.

Goals provide motivation, direction, and purpose for financial resources by giving every dollar a clear mission and turning disciplined saving into an inspiring journey toward the life you truly want. Research in behavioral finance shows people are more likely to stick to a plan when emotionally invested. For example, setting a goal to buy a family home makes regular savings easier. The anticipated long-term benefit outweighs short-term temptations. Visualizing specific outcomes, like becoming debt-free, funding key life events, or enjoying retirement, encourages the commitment needed for consistent, prudent financial choices.

6. Goals enable effective course correction

Financial plans must adapt to life changes, such as job loss, inheritance, illness, marriage, or the arrival of children. When goals are clearly stated and quantified, you can identify which events impact the plan. This helps you adjust contributions, timelines, or expectations as needed. Without documented goals, there is no benchmark to measure progress or determine when changes are necessary.

7. goals help to REDUCE Financial Stress and Anxiety

Planning and saving via Goals Directly Lowers Financial Anxiety

By aligning spending decisions with specific objectives (e.g., building an emergency fund), individuals feel more prepared for the future, which diminishes worry about long-term security. This structured approach turns vague fears into actionable steps. Planning and saving for the future reduces financial anxiety.

Uncertainty breeds fear. When you have written goals and a plan to achieve them, you replace “What if I run out of money?” with “I’m on track to have $1.2M by 2038.” Goals replace worry with confidence.

Conclusion

Establishing goals is a fundamental element of financial planning. Without a definite target and timeframe, even the most advanced investment or tax plans become ineffective. A robust financial plan must start with a well-defined, prioritized, and measurable set of objectives. This solid groundwork is crucial for other strategies to be genuinely effective. Begin by setting your goals—everything else will align from there.